US Housing Market Forecast 2021: Will It Crash or Boom?

We Made the List! (America’s Fastest-Growing Private Companies)

Here are the latest housing market predictions and forecasts for 2021 & 2022. The global pandemic shattered the world order and the US economy suffered its biggest blow since the Great Depression in the second quarter. It has been roughly one year when it put the housing market on hold for several months last spring. Back in March of 2020, the real estate market looked to be headed into a steep decline due to widespread stay-home orders.

Since then, homebuyers, supported by low-interest rates, have kept the housing market afloat. The pandemic has certainly affected every sector but residential real estate has been very resilient. The real estate sector has also been highly supportive of the economic recovery of the country. It has emerged as a pillar of support for the economy. 2020 was a record-breaking year for the US housing market.

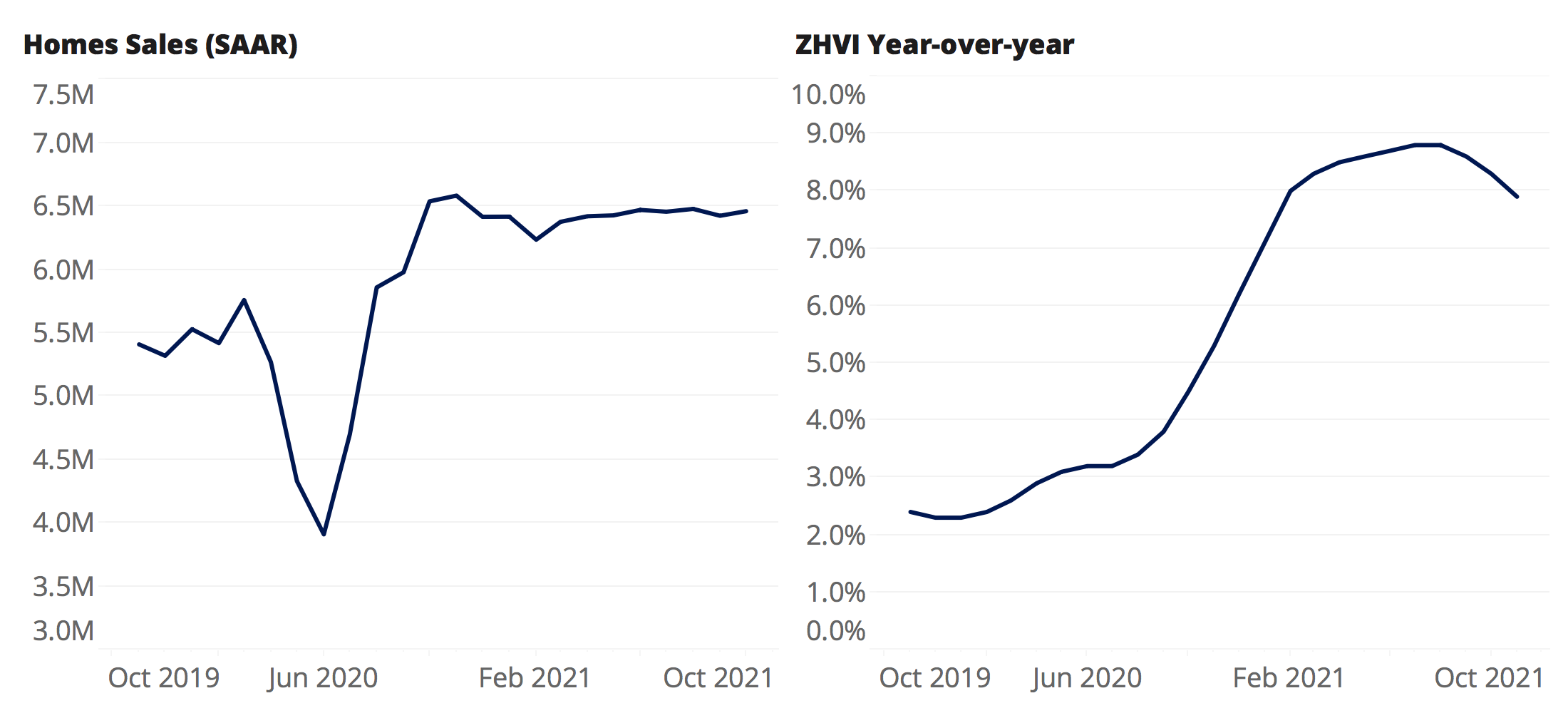

The typical U.S. home was worth $266,104 in December, up 8.4% (or $20,587) from a year ago. A total of 5.64 million homes were sold in 2020, up 5.6% from 2019 and the most since before the Great Recession, according to Lawrence Yun, NAR’s chief economist. Sales also rose 0.7% from November and 22.2% year over year. Existing home sales reached the highest level in 13 years.

The 2021 housing market will continue to be super-competitive for home buyers. The market trends in January 2021 show that home buyers will face a competitive spring season as inventory remains low. House prices in all the major local real estate markets continue to rise. The housing market is becoming harder for home buyers. The demand is really high, and the supply and inventory are deficient.

According to economists and market watchers, home values are growing at their fastest pace in a generation, and are showing no signs of slowing down in 2021. Buyers have to face more competition and act more quickly than usual to snag their dream home. That’s how hot the real estate market has been throughout the pandemic. Although millions were laid off or furloughed it didn’t prevent house hunters from buying homes across the nation.

As a result, the housing market saw the highest pace of sales growth since the height of the unprecedented housing boom in 2005. That expansion was driven by negligent lending in the subprime mortgage market and the current housing boom is driven by the intense demand and record-low mortgage rates. Both of these factors were driven by the coronavirus pandemic.

Housing prices had already started rising before the pandemic arrived but the pandemic created a rapid acceleration in double-digits. The housing market has seen record-breaking growth since June after briefly put on hold during the outbreak of the pandemic this spring.

As prices keep climbing month-over-month, it just shows the resilience of the US housing market in the face of an ongoing economic recession. Despite looming economic uncertainty, highly controversial elections, and the aggravated spread of the pandemic, home buyers continue to quickly snatch up the relatively few homes listed for sale.

The pandemic has really knocked down homebuilders’ ability to fill the housing supply as they are running out of land. The housing market has already been running too short of previously owned homes. The number of homes for sale has plummeted and remained down around 30 percent of what it has been in recent years — leaving the market with nearly twice the demand and two-thirds of the supply.

Both the inventory of homes and mortgage rates are now at their historic lows. The months’ supply of existing homes for sale has fallen to 1.9 months, the lowest level since the series began in 1999. With inventories this tight, it is unlikely that existing home sales can continue to rise at last year’s pace, which means there could be a little slowdown in existing sales throughout 2021. ESR Group expects home sales to rise 3.8 percent in 2021.

The rise in remote work has also sparked a new suburban boom and the scarcity of developed land means that builders could be unable to meet the rising demand and home prices would continue to rise in 2021. One thing that has been talked about a lot is that suburban housing markets are booming because of outbound migration from cities. The pandemic has caused some homebuyers to search for homes in a different area than originally planned.

Various surveys indicate that interest in rural areas and suburbs is up and interest in urban areas is down. However, Zillow published an exhaustive study examining every conceivable housing-market data point related to cities and suburbia to see if there are major divergences that suggest an urban-to-suburban migration trend.

According to that study, suburban housing markets have not strengthened at a disproportionately rapid pace compared to urban markets. Both region types appear to be hot sellers’ markets right now – while many suburban areas have seen a strong improvement in housing activity in recent months, so, too, have many urban areas.

Nevertheless, the pandemic has increased the desire for houses with a bit more space and a garden. Couple that with record-low interest rates, and prices are rising dramatically all over the country from urban-to-suburban markets.

Housing Price Forecast 2021: The Pace of Appreciation is Steady

For now, there are no indications that price growth is going to slow. Zillow Economic Research predicts that home values will increase by 3.6% in the next three months until Feb 2021. Another forecast of theirs is that annual home value growth will rise as high as 13.5% by mid-2021 and for home values to end 2021 up 10.5% from their current levels.

The current forecast also calls for sales volume to remain elevated in the coming year, finishing 2021 at 6.9 million sales, the most since 2005. In previous forecasts, the company predicted a 4.8 percent increase in home values between August 2020 and August 2021. The current extreme demand that is reflected in sharply rising prices, can be attributed to the pent-up demand for home purchases from the March-July period when a great part of the country was in total lockdown.

The housing sales and prices have stayed strong through the fall and winter months amid increasingly short inventory and high demand. Existing home sales also show the tightest housing market on record. The demand has not gotten significantly shorter since last May/June, and buyers and sellers are continuing to connect at a record pace. December existing-home sales rose 0.7% from November.

This trend shows that the housing market is as strong as it was during the housing bubble. It is nowhere too close to a level where you can imagine the balance real estate market conditions. Speedy home sales continue in all regions of the country and the median sales price continues to have double-digit growth. The flow of buyers and sellers has remained abnormally high in the entire fall season.

Not only the housing demand but the supply of new listings has also reached the highest point since the onset of the pandemic. Although sellers are listing more & more homes we need more new home supply to add to inventory and slow these sharp price increases.

As was expected, real estate activity was much better this holiday season compared to last year. Realtor.com’s January 2021 housing data release shows that listing prices continued to increase at double-digit rates compared to last year, fueled by buyer demand, which also continued to snap up homes at a rate almost two weeks more quickly than last year. Whether this momentum can be sustained depends on more inventory becoming available as well as any movement in interest rates, which are expected to slowly tick up in 2021.

- National inventory declined by 42.6% over last year.

- The inventory of newly listed properties declined by 23.2% nationally and by 17.3% for large metros over the past year.

- The January national median listing price was $346,000, up 15.4% compared to last year. Large metros saw an average price gain of 10.9% compared to last year.

- Nationally, the typical home spent 76 days on the market in January, 10 days less than the same time last year.

This January, the national inventory of homes for sale has reached a new low. Homebuyers may need to prepare for a competitive season with lower inventory (especially in more affordable price categories), continuing growth in asking prices in response to strong buyer demand, and slowly rising interest rates. Buyer demand remains far more recovered than supply and continues to grow.

With supply-constrained and demand boosted, house prices seem to rest on solid foundations for next year. They are likely to hold up even if there is a decline in transaction activity in the coming months. This steadiness suggests despite improvements in the trend of new sellers, the current trend gives no relief to buyers because it would not slow down the price growth.

Steady declines in active inventory especially in the face of an improving new listings growth trend suggest that buyers are quickly putting offers on homes. The housing market continues to favor sellers. With high interest from buyers and a limited flow of new listings, the total active listings have been lagging from the previous year.

Homes are being sold at an increasingly fast pace when compared to the previous year. The typical home spent 76 days on the market this December, which is 10 days less than last year.

As new inventory comes on to the market. they are quickly taken out of the market from heavy buyer competition. Therefore, housing units are still in short supply with unsold inventory sitting at a 1.9-month supply at the current sales pace.

Housing Affordability Crisis in 2021

Housing Affordability is driven largely by the gap between household income and home value. It is influenced by the balance between housing supply and demand, the labor market, and mortgage rates by way of Federal monetary policy. Housing is affordable when the housing of an acceptable minimum standard can be obtained and retained leaving sufficient income to meet essential non-housing expenditure.

The most commonly used indicator in the US and many other countries is the ratio of house prices to incomes or earnings. A higher ratio indicates relatively more affordability. A ratio of 100 indicates that median-family income is just sufficient to purchase the median-priced home. Ratios above 100 indicate that the typical household has more income than necessary to purchase the typical house.

Therefore, low-income households spending a high proportion of their income on housing may and vice versa.

The combination of intense demand and the low mortgage rates has pushed home prices to levels that are making it difficult to save for a down payment, particularly among first-time buyers. While we still face economic and health challenges ahead, it is no doubt that the nation will continue to recover from this pandemic and an improving economy will continue to prop up the housing market competition. Industry experts believe the housing market will remain strong and is set to break more records in 2021.

Various national surveys (which you can read below) show that consumers are eager to spend more on housing in 2021, as the economy continues to slowly recover from the pandemic. Strong growth is expected in 2021 for housing sales, rents, and home prices. A report from the Federal Reserve Bank of New York found that the median household expects to increase their spending by 3.7% in the next twelve months, the most optimistic outlook since 2016.

This time the housing market is largely being driven by two factors: a shortage of available housing inventory and extremely low-interest rates. Double-digit annual growth in both list and sale prices show an extreme lack of inventory and incredible demand — A sign of a seller’s real estate market. The housing market is still hot, but we may be starting to see rising home prices hurting affordability unless the mortgage rates continue to decline in 2021.

Mortgage rates have risen slightly from the trough seen in early January, but they continue to be historically low, which should support mortgage demand. Mortgage applications decreased 4.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 5, 2021. The Refinance Index decreased 4 percent from the previous week and was 46 percent higher than the same week one year ago.

Mortgage rates have increased in four of the first six weeks of 2021, with jumbo rates being the only loan type that saw a decline last week. Despite some weekly volatility, Treasury rates have been driven higher by expectations of faster economic growth as the COVID-19 vaccine rollout continues,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 2.97 percent from 2.94 percent, with points increasing to 0.36 from 0.29 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week. Despite house mortgage rates being less than 3%, housing affordability has decreased because the effect of lower mortgage rates (for buyers) is being evened out by double-digit home price growth.

In 2021, mortgage rates are expected to stop dropping. Rather, the National Association of Realtors expects rates to average 3.1% and the Mortgage Bankers Association says mortgage rates will average 3.3% in 2021. These rate estimates are both up from the 3.0% mortgage rate average in 2020 but lower than 2019 average rates.

The combination of rising mortgage rates and increasing home prices will accelerate the decline in affordability and further squeeze potential home buyers during the spring home sales season. Mortgage rates have increased in four of the first six weeks of 2021. Expect mortgage rates to continue to hover around record lows. The Federal Reserve has reassured that it will keep interest rates and its bond-buying program unchanged — downplaying any urgency to bring borrowing costs back up from their lowest levels in history at near zero.

According to Bankrate’s latest survey of the nation’s largest mortgage lenders, as of Feb 15, the average 30-year fixed-mortgage rate is 2.86 percent, an increase of 1 basis point since the same time last week. A month ago, the average rate on a 30-year fixed mortgage was higher, at 2.89 percent.

At the current average rate, you’ll pay principal and interest of $414.09 for every $100,000 you borrow. Compared to last week, that’s $0.53 higher. A year ago, the 30-year fixed-rate, was 3.70 percent, so you would have paid $460 each month for the same amount. The average 15-year fixed-mortgage rate is 2.34 percent, down 1 basis point since the same time last week. Monthly payments on a 15-year fixed mortgage at that rate will cost around $659 per $100,000 borrowed.

According to Realtor.com, the median listing prices grew at 15.4 percent over last year to reach $346,000 in January, notching 25 consecutive weeks of double-digit price growth. This growth rate is higher than December’s growth rate of 13.4%. With demand still high and supply still limited, this path seems unlikely to change in the coming months. 2021 real estate market is predicted to remain sizzling hot affecting housing affordability.

So, for now, we have a median price of $346,000 and a 30-year fixed mortgage rate of 2.860%. Assuming a buyer provided a 20% down payment, the principal and interest payments on the mortgage would have been $1,146 a month.

Contrast that with December 2019, when the median price was $299,995 and the average interest rate on a 30-year mortgage was around 3.58%, according to Freddie Mac. A buyer faced a payment of $1,088, or $58 less a month than what he is paying now. Assume that builders and sellers had met buyer demand, keeping prices flat over the year.

Lower mortgage rates would have resulted in a monthly payment of $993, or a savings of $95 a month as compared to a year before. As you can see, low mortgage rates help but don’t eliminate the risk of affordability crunch that the housing market could still face if home prices continue to rise at a rapid pace.

Buying a home in a seller’s market can feel like you’re losing money. You may just wait a few months or even a year so that prices will flatten (or come down). The problem is that prices could keep rising to the point where you’re priced out of the market. There’s no guarantee either way.

Therefore, we feel this is the right time to buy your dream property or you can opt to refinance at today’s rates to at least cut your monthly mortgage payments. The present scenario makes it appealing to buyers who have been spending all this money on rent.

Housing Market and Mortgage Delinquencies 2021

Record-low mortgage rates and shortage of inventory are keeping the US housing market strong concerning buyer demand. Prices have been surging month-over-month breaking new records. The government’s moratoria have effectively stopped foreclosure activity on everything but vacant and abandoned properties. 2020 ended the year with a near-record number of seriously delinquent loans, but historically low levels of foreclosure activity.

There is a backlog of foreclosures building up due to this moratorium and no one knows how big that backlog is until after the government programs expire. The foreclosure backlog comprises three types of loans — loans that were in foreclosure before the government’s moratoria; loans that would have defaulted under normal circumstances; and loans that would default due to job losses induced by the pandemic.

To help borrowers at risk of losing their home due to the coronavirus national emergency, the Federal Housing Finance Agency (FHFA) announced that Fannie Mae and Freddie Mac (the Enterprises) will extend the moratoriums on single-family foreclosures and real estate owned (REO) evictions until February 28, 2021.

It will give relief to more than 28 million homeowners with an Enterprise-backed mortgage. The foreclosure moratorium applies to Enterprise-backed, single-family mortgages only. The REO eviction moratorium applies to properties that have been acquired by an Enterprise through foreclosure or deed-in-lieu of foreclosure transactions. The current moratoriums were set to expire on January 31, 2021.

Per the last three extensions, the FHFA said it will continue to monitor the effect of coronavirus on the mortgage industry and update its policies as needed. Currently, FHFA projects additional expenses of $1.4 to $2 billion will be borne by the Enterprises due to the existing COVID-19 foreclosure moratorium and its extension.

Mortgage delinquencies improved in December 2020 but 2020 ended with 1.7 Million more seriously delinquent homeowners than at the start of the year, according to the latest data released by Black Knight.

- Despite the year-over-year increase, the national delinquency rate saw a modest improvement in December, falling by 3.9% from November to 6.08%, the lowest level since April 2020

- Serious delinquencies (loans 90 or more days past due) also improved, falling to 2.15 million from 2.19 million the month prior

- Even after months of improvement, 90-day default activity rose by more than 250% (+2.6 million) overall in 2020

- Foreclosure starts fell by 67% from the year prior and the year’s 40,000 foreclosure sales (completions) represented an annual decline of more than 70%

- Starts and sales have hit record lows as moratoriums and forbearance plans protect distressed homeowners from facing foreclosure in the wake of the pandemic

- Prepayment activity rose by 12% in December, ending the year 112% higher than the same month in 2019 and highlighting a still-strong refinance market entering 2021

ATTOM Data Solutions, licensor of the nation’s most comprehensive foreclosure data released its Year-End 2020 U.S. Foreclosure Market Report. The report shows that foreclosure filings (default notices, scheduled auctions, and bank repossessions) were reported on 214,323 U.S. properties in 2020, down 57 percent from 2019 and down 93 percent from a peak of nearly 2.9 million in 2010, to the lowest level since tracking began in 2005.

Those 214,323 properties with foreclosure filings in 2020 represented 0.16 percent of all U.S. housing units, down from 0.36 percent in 2019 and down from a peak of 2.23 percent in 2010. The report also includes new data for December 2020, showing there were 10,876 U.S. properties with foreclosure filings, up 8 percent from the previous month but down 80 percent from a year ago.

Bank repossessions decrease 95 percent since their peak in 2010. Lenders repossessed 50,238 properties through foreclosure (REO) in 2020, down 65 percent from 2019 and down 95 percent from a peak of 1,050,500 in 2010, to the lowest level as far back as data is available — 2006.

States with the highest foreclosure rates in 2020 were Delaware (0.33 percent of housing units with a foreclosure filing); New Jersey (0.31 percent); Illinois (0.30 percent); Maryland (0.26 percent); and South Carolina (0.24 percent).

Rounding out the top 10 states with the highest foreclosure rates were Florida (0.23 percent); Connecticut (0.22 percent); Ohio (0.21 percent); Georgia (0.19 percent); and Indiana (0.18 percent).

Metro areas with a population greater than 1 million that had the highest foreclosure rate, were, Cleveland, Ohio (0.34 percent); Chicago, Illinois (0.30 percent); Baltimore, Maryland (0.29 percent); Philadelphia, Pennsylvania (0.29 percent); and Riverside, California (0.28 percent).

New Single-Family Housing Construction Trends

The NAHB gets input from builders on how confident they are in the housing market based on buyer behavior, sales, and incorporates any forecasts as well. The building permits have rebounded from pandemic lows and builders are racing to fill the gap between supply and demand.

Rising material costs led by a huge upsurge in lumber prices, along with a resurgence of the coronavirus across much of the nation, pushed builder confidence in the market for newly-built single-family homes down three points to 83 in January, according to the latest NAHB/Wells Fargo Housing Market Index (HMI). Despite the drop, builder sentiment remains at a strong level.

All three major HMI indices fell in January. The HMI index gauging current sales conditions dropped two points to 90, the component measuring sales expectations in the next six months fell two points to 83 and the gauge charting traffic of prospective buyers decreased five points to 68. Looking at the three-month moving averages for regional HMI scores, the Northeast fell six points to 76, the Midwest was up two points to 83, the South fell one point to 86 and the West posted a one-point loss to 95.

The decline in homebuilder sentiment in January and the sharp drop in new home sales in November suggests that single-family starts may decelerate in the near-term from the current impressive pace. The demand for home purchases remained strong in mid-January, as purchase mortgage applications hit a 12-year high.

“Despite robust housing demand and low mortgage rates, buyers are facing a dearth of new homes on the market, which is exacerbating affordability problems,” said NAHB Chairman Chuck Fowke. “

“While housing continues to help lead the economy forward, limited inventory is constraining more robust growth,” said NAHB Chief Economist Robert Dietz. “A shortage of buildable lots is making it difficult to meet strong demand and rising material prices are far outpacing increases in home prices, which in turn is harming housing affordability.”

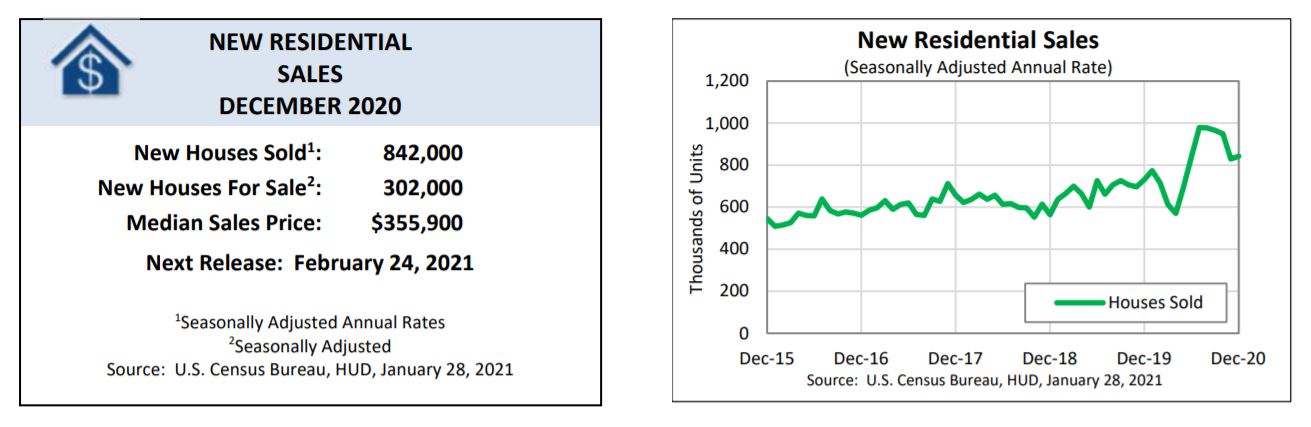

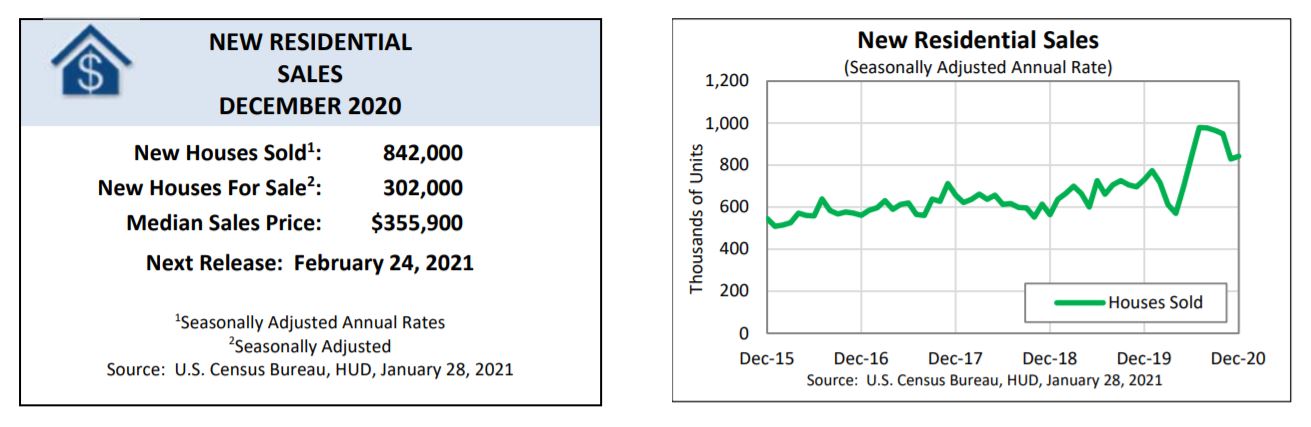

New Residential Home Sales: December 2020

Sales of existing home sales are at an all-time high but new home sales have also risen during the pandemic. Those sales are allowing builders to raise prices. Buyer traffic is converting into sales at a record rate. According to Urban Land Institute, real estate market conditions and values in the U.S. are expected to rebound in 2021 and trend even higher in 2022, with single-family homes outperforming other sectors such as commercial, retail, hotel, and rental.

New single-family construction starts will fall slightly to 871,250 in 2020 before rising to 940,000 in 2021 and 975,000 in 2022, the highest level since 2006. In the meantime, home prices will grow an average of 4.1% over the next three years, above the long-term average of 3.9%, according to the report, based on a survey of 43 economists at 37 leading real estate organizations.

An estimated 811,000 new homes were sold in 2020. This is 18.8 percent (±4.3 percent) above the 2019 figure of 683,000. Sales of new single-family houses in December 2020 were at a seasonally adjusted annual rate of 842,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 1.6 percent (±15.8 percent) above the revised November rate of 829,000 and is 15.2 percent (±17.2 percent) above the December 2019 estimate of 731,000.

The median sales price of new houses sold in December 2020 was $355,900. The average sales price was $394,900. The seasonally-adjusted estimate of new houses for sale at the end of December was 302,000. This represents a supply of 4.3 months at the current sales rate.

Courtesy of Census.gov

Till the time coronavirus pandemic exists it will lead to a see-saw recovery with ups and downs. Let us discuss in detail the various housing indices & their predictions for 2021 & 2022. We have updated this article with the latest housing market report from various credible sources like Realtor.com (check reference section).

National Multifamily Housing Trends

The multifamily industry continues to face steep challenges brought in by the pandemic. The federal government has included $25 billion as rental assistance in the recently passed COVID relief package. The National Multifamily Housing Council (NMHC)’s Rent Payment Tracker found 88.6 percent of apartment households made a full or partial rent payment by January 20 in its survey of 11.6 million units of professionally managed apartment units across the country.

This is a 2.5 percentage point, or 294,224 household decrease from the share who paid rent through January 20, 2020, and compares to 89.8 percent that had paid by December 20, 2020. These data encompass a wide variety of market-rate rental properties across the United States, which can vary by size, type, and average rental price.

As you read further, we have collected some data from credible sources that show how the US housing market is recovering week after week from the blows of the pandemic.

Housing Market Crash or Boom in 2021?

The US housing market is far from crashing in 2021 or 2022. In fact, it continues to play an important supportive role in the country’s economic recovery. Current economic conditions resemble a “swoosh” pattern, with the initial impact from the lockdown followed by a gradual recovery as the economy reopens.

Mortgage rates and slow but steady improvements to the job landscape continue to propel confidence for first-time buyers. The pace of existing-home sales has jumped to a level not seen since 2006 and, importantly, was followed by strong pending sales, purchase mortgage applications, and construction data.

The U.S. economy is expected to grow 5.3 percent in 2021, a substantial improvement from the currently projected 2.7 percent contraction in 2020, with a strong pick-up in growth projected to commence over the spring months, according to the latest commentary from the Fannie Mae (FNMA/OTCQB) Economic and Strategic Research (ESR) Group.

Housing activity is expected to remain strong in 2021, but the growth will likely decelerate from the torrid pace set in the second half of 2020. While the ESR Group expects home sales to rise 3.8 percent in 2021, the monthly pace is likely to slow through much of the year. Home price appreciation is also expected to slow along a similar timeline.

Historically, low-interest rates are also an inducement to buy homes, but slow supply growth continues to result in high levels of home price appreciation, which is offsetting some of the affordability benefits of the lower rate environment. Housing starts have surpassed expectations at the end of 2020 and remain poised to show continued strength in 2021.

The latest forecast of full-year 2021 real GDP growth is an upgrade of 0.8 percentage points from the previous month’s forecast, reflecting the ESR Group’s view that the expansion of COVID-19 vaccination efforts and the approach of warmer weather will likely reverse the economic weakness experienced at the end of 2020.

As Federal Reserve has made clear that it has no intention of raising interest rates soon, many households are seizing the opportunity to refinance their existing mortgages. Let’s first see how various consumer surveys are responding in wake of this crisis.

The Fannie Mae Home Purchase Sentiment Index® (HPSI) is a good indicator of the houisng recovery and buyer and seller behavior. The index measures housing attitudes, intentions, and perceptions, using six questions from the National Housing Survey® (NHS). The HPSI fell for the second straight month in December to 74.0, a 6.0 point decline from November.

Five of the six HPSI components decreased month over month, and consumers reported a substantially more pessimistic view of homebuying and home-selling conditions, which drove the relatively large monthly change. Year over year, the HPSI is down 17.7 points. It fell 1.7 points in November to 80.0, the first decline after three consecutive months of increases since late spring.

The sell-side component fell for the first time since April and by 18 points which shows a more pessimistic view of home-selling conditions and home prices, including mortgage rate expectations. If sellers choose to wait to list their homes, this could have the effect of perpetuating already-tight inventory levels and supporting additional home price growth, which could contribute to a further moderating of home sales and decreasing housing affordability.

The latest survey finds out the percentage of respondents who think it’s a ‘good/bad time to sell a home’ vs those who think it’s a ‘good/bad time to buy a home’.

- Good/Bad Time to Buy: The percentage of respondents who say it is a good time to buy a home decreased from 57% to 52%, while the percentage who say it is a bad time to buy increased from 35% to 39%. As a result, the net share of Americans who say it is a good time to buy decreased 9 percentage points month over month.

- Good/Bad Time to Sell: The percentage of respondents who say it is a good time to sell a home decreased from 59% to 50%, while the percentage who say it’s a bad time to sell increased from 33% to 42%. As a result, the net share of those who say it is a good time to sell decreased 18 percentage points month over month.

- Home Price Expectations: The percentage of respondents who say home prices will go up in the next 12 months remained the same at 41%, while the percentage who say home prices will go down increased from 13% to 16%. The share who think home prices will stay the same decreased from 35% to 34%. As a result, the net share of Americans who say home prices will go up decreased 3 percentage points month over month.

- Household Income: The percentage of respondents who say their household income is significantly higher than it was 12 months ago decreased from 24% to 20%, while the percentage who say their household income is significantly lower remained unchanged at 18%. The percentage who say their household income is about the same increased from 57% to 61%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago decreased 4 percentage points month over month.

The Federal Reserve Bank of New York’s Center for Microeconomic Data released the December 2020 Survey of Consumer Expectations, which shows that median inflation expectations increased at the medium-term horizon, and remained unchanged at the short-term horizon. Uncertainty about future inflation increased slightly, remaining at an elevated level.

Median home price change expectations, which have been trending upward after reaching a series’ low of 0% in April 2020, increased sharply from 3.0% in November to 3.6% in December, the highest reading since July 2018.

It also shows that mean unemployment expectation — or the mean probability that the U.S. unemployment rate will be higher one year from now — decreased from 40.1% in November to 38.9% in December, equal to its trailing 12-month average.

The mean perceived probability of losing one’s job in the next 12 months increased slightly from 14.6% in November to 15.0% in December, remaining slightly below its December 2019 level of 15.4%. Median expected household income growth increased by 0.1 percentage point to 2.2% in December.

According to Zillow’s market pulse report dated February 12, 2021, housing market sentiment improved in January, while overall economic optimism remained depressed. While demand for housing remains red hot, supply-side constraints that have hindered homebuilders for years have recently become even more acute. Mortgage rates are holding firm even as Treasury yields continue to rise and access to most mortgages became easier in January.

- More existing homes were sold in 2020 than in any year since 2006

- December existing-home sales rose 0.7% from November and 22.2% from December 2019 to 6.76 million (SAAR).

- In total, 5.64 million homes were sold in 2020, up 5.6% from 2019.

- Home value growth breaks new records.

- The typical U.S. home was worth $266,104 in December, up 8.4% (or $20,587) from a year ago.

- Home values grew 3.2% in the fourth quarter of 2020 – the fastest three-month pace of appreciation since at least 1996.

- December housing starts cap an extraordinary year

- December housing starts rose 5.8% from November and 5.2% from a year ago to 1.669 million (SAAR).

- The 1.709 million (SAAR) permits filed in December were up 4.5% and 17.3%, respectively, from November and December 2019.

- Home values in Austin grew 5.3% in the past quarter, while home values grew 5.1% over the same period in Phoenix, San Diego, and Salt Lake City.

- For now, there are no indications that price growth is going to slow.

- Zillow’s latest forecast predicts annual home value growth will rise as high as 13.5% by mid-2021, and for home values to end 2021 up 10.5% from their current levels.

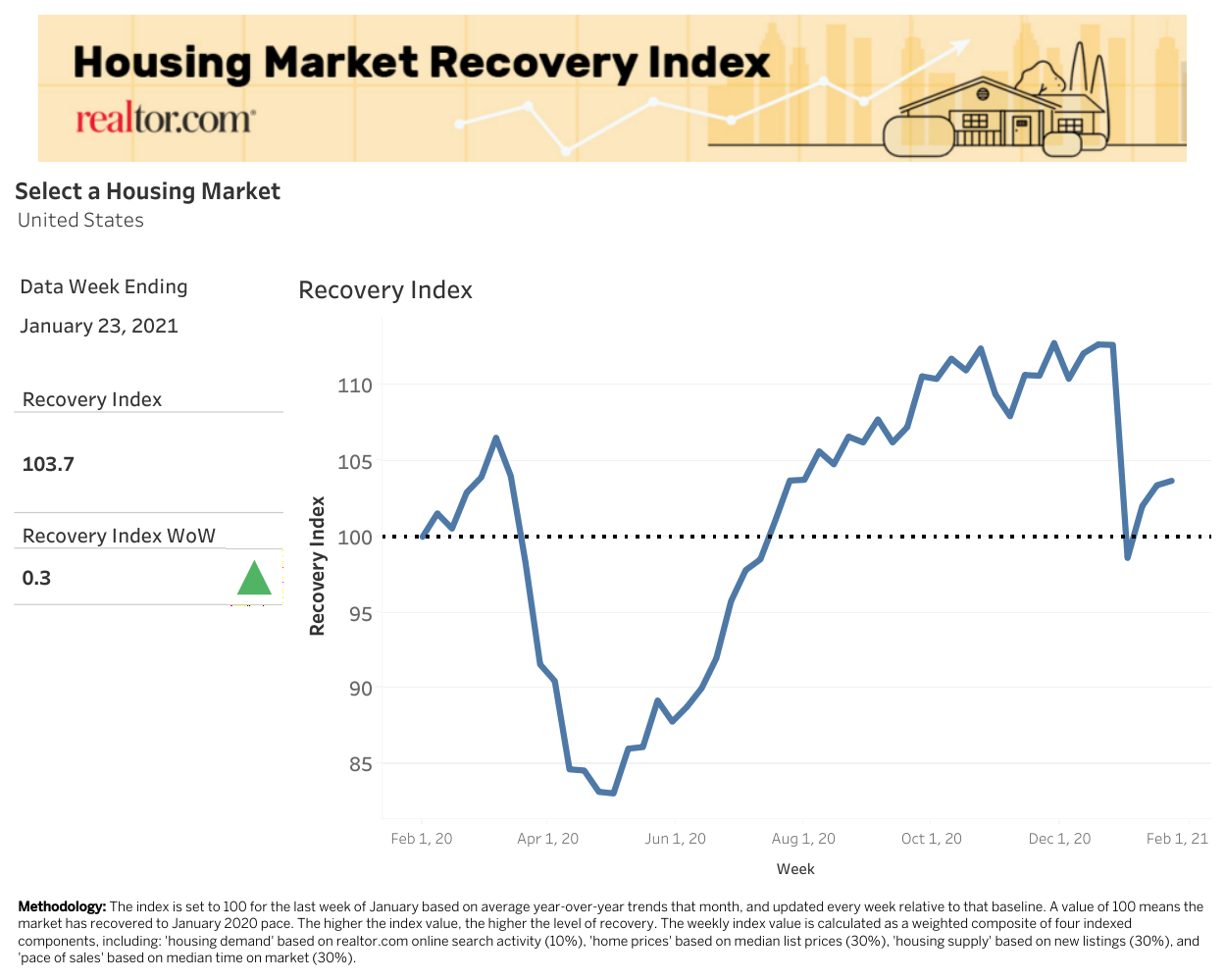

Realtor’s Recovery Index: No Housing Market Crash Coming

According to Realtor.com’s latest recovery report, the Housing Market Recovery Index reached 103.7 nationwide, up 0.3 points over the prior week.

- The overall index remains above the pre-COVID baseline, with all measures growing faster than this time last year, except for new listings.

- The ‘housing demand’ component increased 2.1 points to 116.9, growing but at a slower pace than in December.

- The overall recovery index is showing the greatest recovery in Portland, Los Angeles, Denver, Boston, and Las Vegas.

| Week ending 1/23 | Current Index | w/w Change |

| Overall Housing Recovery Index | 103.7 | +0.3 |

| Housing Demand Growth Index | 116.9 | +2.1 |

| Listing Price Growth Index | 110.8 | -0.6 |

| New Supply Growth Index | 87.3 | +0.8 |

| The pace of Sales Index | 108.6 | +0.0 |

The graph below charts the index by showing how the real estate market started strong in early 2020, and then dropped dramatically at the beginning of March when the pandemic paused the economy. It also shows the strength of the recovery since the beginning of May. A W-shaped recovery can be seen.

Credits: Realtor.com (Housing Market Recovery Index)

The housing index is pegged to a starting point of 100 at a particular year. And then they can just track whether things are improving or declining from that reference point. It’s similar to any other index where you have a starting point or a starting year and you peg it at a hundred and it just goes up and down from there.

It went up for most of March, and then it hit this peak and came down rapidly and fast over the course of essentially the end of March, April, and right through to the beginning of May where it bottomed out. So after May 1st, that index started to go up, it passed 85 in mid-May and then continue to work its way up rather quickly.

The recovery index had reached 106.6 nationwide for the week ending July 18, bringing the index above the pre-COVID recovery benchmark for the first time since March, and then it kept going up from there till Dec 26.

After that, it fell sharply by 14.1 points and reached below the pre-COVID benchmark on Jan 2, 2021. It was the first major decline that we have seen since April 2020. The index has formed a V-shaped curve back again reached 103.7 points as of Jan 23.

Are Housing Prices Increasing?

Last year, the inflow of buyers and sellers remained abnormally high. The ‘home price’ component fell slightly to 110.8 points this past week but remains well above the January 2020 baseline and remains higher than the 109.7 point average over the course of December. With inventory failing to see any visible improvement, asking prices continue to rise near-record levels even as short-term economic and COVID concerns fail to disappear. Sellers have newfound leverage, enabling the fastest listing price growth recorded in more than two years.

Although the fastest price growth has been recorded since January 2018 it is yet to be seen whether higher asking prices will translate into higher selling prices. A seller would always prefer sales to a list price ratio of 100% or more. If inventory continues to decline at the current sales pace, we’ll get a clear indication of this ratio.

Locally, 33 of the 50 largest houisng market markets seeing growth in asking prices surpass the January baseline, the same as the previous week. The most recovered markets for home prices include Austin, Pittsburgh, Riverside, Richmond, and Houston, with a home price growth index between 113 and 128.

Is The Housing Demand Growing?

The Housing Demand component – which tracks growth in online home searches nationwide – increased to 116.9 this past week, up 2.1 points over last week but still down compared to the 122.9 point average over the course of December. It shows that the pool of active buyers has continued to grow but at a visibly slower rate than observed in the fall. Buyers remain motivated but watchful of interest rates and frustrated by a shrinking inventory.

Locally, 45 of the 50 largest real estate markets are still positioned above the recovery trend, up by 3 from the previous week. The most recovered markets for home-buying interest include Austin, Miami, Houston, San Antonio, and Seattle; with a housing demand growth index between 137 and 153.

Is Housing Supply Increasing?

In the first week of August, the index had managed to reach the January baseline for the first time as more sellers re-entered the market but it was a temporary boost in new listings which weakened later in August. The housing supply index, which measures the growth of new listings, has been slow to recover in the first two weeks of the new year but continues to move slowly in the right direction.

Last week, the supply component rose slightly to 87.3, 0.8 points above the previous week but still down compared to the 107.6 point average over the course of December. Selling activity has remained volatile in the post-pandemic period, and this relatively slow start to the year by sellers confirms that they might wait to list more homes.

A sustained rebound in newly listed homes for sale remains elusive and highly localized but this week’s improvement is encouraging. The housing supply will need to carry consistent momentum forward to balance the relentless growth in demand.

Will sellers choose to go against the usual seasonal decline in new listings? What do you think? Locally, only 11 of the 50 largest housing markets saw the new listings index remain above the January baseline, two fewer than the previous week.

Interestingly, markets, where new supply is improving the fastest, tend to be higher priced than those that have yet to see improvement, suggesting sellers are more active in the more expensive markets. A failure of new listings to improve beyond the current pace could prove to be an obstacle for further sales improvements, given their strong correlation with sales.

The most recovered markets for new listings included San Jose, Denver, San Francisco, Los Angeles, and Las Vegas, with a new listings growth index between 115 and 137. While San Jose and San Francisco’s new listings still outpace January 2020, it’s worth noting that the pace of new listings growth is down considerably compared to December in these metros, which has had a large impact on their recovery scores this week.

Houisng markets where new supply is improving the fastest, tend to be higher priced than those that have yet to see improvement, suggesting sellers are more active in the more expensive markets. More homes being listed for sale in areas with wealthier demographics goes some way to explain the strength of the housing market at a time of recession and rising unemployment.

Are Housing Sales Recovering?

Home sales are recovering from the setback of the coronavirus-led crisis with fall becoming the peak homebuying season. The pace of sales component – which tracks differences in time-on-market – held well above the pre-COVID baseline at 108.6, the same as the previous week but lower than the 114.9 point average over the course of December.

Despite the moderate deceleration, homes continue to move at a record pace for this time of the year and faster than in pre-pandemic times. In other words, homes are selling faster than the same time last year.

Locally, 43 of the 50 largest housing markets in the US are now seeing the time on market index surpass the January baseline, the same as the previous week. The most recovered markets for time-on-market include Los Angeles, Portland, Riverside, Louisville, and Phoenix; with a pace of sales growth index between 135 and 151.

This past week, San Jose and San Francisco saw their ‘pace of sales’ scores fall well below the recovery point. While the time spent on the market in these metros has not significantly risen, it has failed to keep up with the blistering drop-in time on the market seen in late January and early February 2020, right before the onset of the pandemic.

Are Housing Rents Declining?

The rental market appears poised to turn the corner and demand for rental units is expected to surge in 2021. While rising rents is a good sign for rental property owners, it will certainly put millions of renters hit hard by pandemic-related income loss in an even more difficult position, and further government intervention will likely be needed to avoid a painful wave of evictions. In general, there are some significant early signs of trend reversals from what the rental market saw throughout the majority of 2020. These shifts, however, don’t come as a total surprise, as the rental market tends to pick up in the New Year after the holiday season.

Below you’ll find various rent reports that highlight year-over-year rent trends and price fluctuations that renters may be experiencing in various parts of the United States.

December’s data by Realtor.com shows rents across the nation’s largest 100 counties are continuing their slowdown, with year-over-year trends easing since March across the studio, one-bedroom, and two-bedroom units.

- In several major and most expensive cities in the country, rents are down substantially compared to last year.

- The urban tech centers such as the Bay Area, Manhattan, Boston, Seattle, and Washington, D.C all saw the largest declines in rents compared to last year.

- One-bedroom rents were declining year-over-year in 37 of the 100 largest counties, up from just 6 in March.

- Two-bedroom rents were declining year-over-year in 28 of the 100 largest counties, up from just 12 in March.

- San Francisco again topped the list of rent declines in all three unit types with studio rents declining by 33.8 percent, one-bedrooms by 25.5 percent, and two-bedrooms by 22.8 percent.

Apartment List National Rent Report shows that COVID’s impact on the market is continuing to stabilize.

- The most expensive markets saw rents fall rapidly while several more affordable mid-sized cities experienced accelerating rent growth.

- Their national index ticked up by 0.1% from December to January, the first monthly increase since last August.

- Year-over-year, rents are now down by 1.2 percent nationally, a slight increase from the 1.5 percent year-over-year decline that we reported last month.

- Boise ranks #1 for fastest year-over-year growth, with rents up by 12.4 percent.

- The vast majority of that growth in Boise occurred from April through October, and over the past three months, rents in Boise have increased by a total of just 0.4 percent.

- In Chesapeake, VA, rents are up by 8.4 percent year-over-year, but fell by 0.5% this month, the first decline since the start of the pandemic.

Zumper’s National Rent Report (February 2021), shows some early signs of reversing the unprecedented rental market trends we saw throughout 2020.

- Nationally, rents remain slightly up across the country, while expensive coastal cities are still down dramatically compared to a year ago. Nationally, median 1-bedroom rent was up 0.6% from a year ago, and median 2-bedroom rent was up 1.7%.

- The national 1-bedroom median and 2-bedroom median grew 0.3% and -0.1% at a monthly rate, respectively.

- Rents continue to be down considerably in historically expensive, coastal cities from a year ago.

- At the same time, rents in historically cheaper cities throughout the Midwest and Southwest are up considerably from a year ago.

- Bay Area Shows Early Signs of Rent Growth.

- For the first time since April 2020, rental prices are increasing at a monthly rate in San Francisco after months of decline in the city and throughout the entire Bay Area

- The top 8 cities are the 8 most expensive as ranked in the January 2020 report: San Francisco, CA; New York, NY; Boston, MA; Oakland, CA; San Jose, CA; Washington DC; Los Angeles, CA; and Seattle, WA.

- Second-Tier Cities and New Tech Hubs appear to be declining in price somewhat in recent months.

- This group that comprises Miami, FL and Austin, TX, is eager to welcome tech companies and workers that are fleeing traditional tech hubs like San Francisco and New York City.

- These cities have seen a spike in renter searches on Zumper in recent months, which could be a result of price decreases.

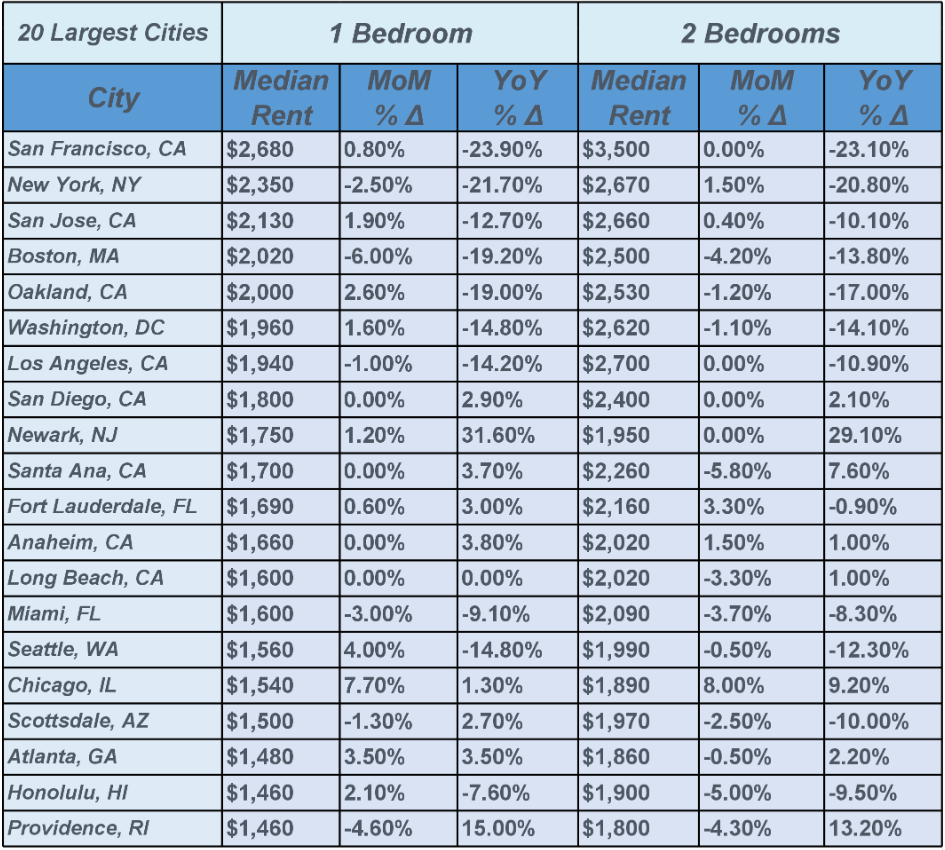

Here’s a snapshot of January 2021 rental prices in the top 20 largest cities in the country.

Source: Zumper National Rent Report

Apartment Guide’s January 2021 Rent Report shows that rents are rising modestly on one-bedroom apartments and more noticeably on two-bedroom and three-bedroom apartments. This may be due to household consolidation as consumers grapple with the economic pressure introduced by COVID-19.

- On a national level, prices on studio apartments are down and one-bedroom units are up modestly. In comparison, both two-bedroom and three-bedroom units are up.

- Studios are down 6 percent from six months ago and down 2.4 percent from one year ago.

- One-bedroom units are down 3 percent from six months ago, but up 1.8 percent year-over-year.

- Two-bedrooms are up 3.8 percent from where they were one year ago.

- Three-bedroom units are up 4.2 percent from where they were one year ago.

- The West and Northeast regions haven’t been on the same trend line for rent prices in recent comparisons — until now.

- In both the West and the Northeast, studio and one-bedroom apartments are less expensive than they were a year ago, while two-bedroom and three-bedroom units are more expensive.

- Of the top 20 cities for rising rent prices across unit types, 31 percent have populations of 500,000 or less.

- That indicates strong momentum in the rental markets of smaller cities, leaving them well-positioned for further growth.

| Bedrooms | 2020 | 2019 | 2018 |

|---|---|---|---|

| Studio | $1,608 | $1,648 | $1,598 |

| 1 | $1,598 | $1,570 | $1,582 |

| 2 | $1,865 | $1,797 | $1,798 |

| 3 | $2,036 | $1,955 | $1,947 |

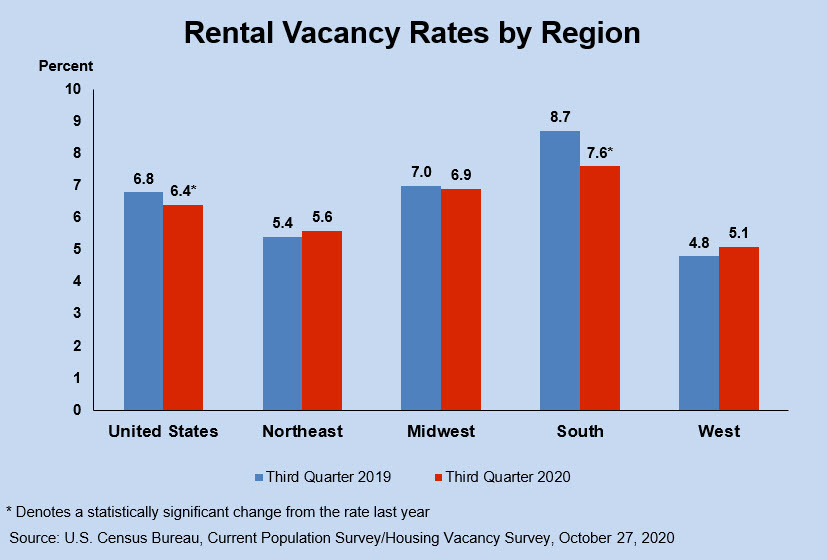

RESIDENTIAL VACANCIES AND HOMEOWNERSHIP RATES Q3 2020

Vacancy rates affect the price of housing. In a market in which there are a lot of vacant homes or apartments, prospective tenants or buyers are at an advantage. On the other hand, in a market in which vacant homes or apartments are scarce, the power dynamic is reversed. The landlords (or sellers) are in a position to tend to bid up the rents.

Therefore, when there is an unusually low vacancy, the price of housing will tend to be bid up over time. When there is an unusually high vacancy, the price of housing will tend to be bid down over time.

Let us see how this pandemic-led economic slowdown has impacted the vacancy rates nationally as well as regionally. The vacancy rate is somewhat analogous to the unemployment rate. If the unemployment rate increases, it has a direct impact on vacancy rates, just as what happened this year since March.

COVID-19 continues to limit economic activity, yielding higher apartment vacancies, and lower overall rent growth. The Census Bureau reports rental vacancy and homeownership vacancy rates each year through its American Community Survey; you can get these at the city level or in some cases for even more fine-grained areas.

According to the U.S. Census Bureau, the homeowner vacancy rate in 2019 was 1.3%, and the rental vacancy rate at approximately 6.8%. In the third quarter of 2020, the national vacancy rates were 6.4 percent for rental housing and 0.9 percent for homeowner housing.

Approximately 89.9 percent of the housing units in the United States in the third quarter of 2020 were occupied and 10.1 percent were vacant. Owner-occupied housing units made up 60.6 percent of total housing units, while renter-occupied units made up 29.3 percent of the inventory in the third quarter of 2020.

It is interesting to see that the rental vacancy rate of 6.4 percent was 0.4 percentage points lower than the rate in the third quarter of 2019 (6.8 percent) and 0.7 percentage points higher than the rate in the second quarter of 2020 (5.7 percent).

10 Rules of Successful Real Estate Investing

And the homeowner vacancy rate of 0.9 percent was 0.5 percentage points lower than the rate in the third quarter of 2019 (1.4 percent) and virtually unchanged from the rate in the second quarter of 2020 (0.9 percent).

On the other hand, the homeownership rate of 67.4 percent was 2.6 percentage points higher than the rate in the third quarter of 2019 (64.8 percent) and not statistically different from the rate in the second quarter of 2020 (67.9 percent).

Usually larger metro areas have an advantage when it comes to rental properties. They have an abundant supply of renters in the high-income bracket with more disposable income who are willing to compete for the best apartments and rentals. However, industry experts are seeing more positive conditions in many suburban markets.

Buyers of apartment properties are returning to the market, spurred by historically low-interest rates and increased equity financing availability. In the third quarter of 2020, the rental vacancy rate was the highest in Metropolitan Statistical Areas (7.5) percent. Also, it was not statistically different principal cities (7.0 percent).

But suburbs had the lowest rental vacancy rate of 5.5 percent, 1.5 percentage points lower than principal cities. According to The New York Times, an estimated 5% of New York City residents and 18% of Manhattanites alone left the city between March and May. Suburbs like Westchester, Long Island, and North Fork have become other popular sanctuaries inside New York State.

This combination of high demand and low supply has driven prices higher in the suburbs. As affluent New Yorkers are buying houses in suburbs, the real estate market in those areas has prospered. In Manhattan, however, the median rental price decreased by 3.9% between August 2019 to August 2020, and the vacancy rate has increased by 3.15%.

The third quarter 2020 rental vacancy rate in the Northeast (5.6 percent) was lower than the rates in the Midwest (6.9 percent) and South (7.6 percent), but it was not statistically different from the rate in the West (5.1 percent).

The rental vacancy rates in the Midwest and South were higher than the rate in the West, and there was not a significant difference between the rates in the Midwest and South.

The rental vacancy rate in the South was lower than the third quarter 2019 rate, while the rental vacancy rates for the Northeast, Midwest, and West were not statistically different from the third quarter 2019 rates.

Courtesy of Census.gov

The third quarter 2020 homeownership rates in the Midwest (71.2 percent) and South (70.8 percent) were higher than the rates in the Northeast (62.0 percent) and West (62.1 percent). The rates in the Midwest and South were not statistically different from each other, nor were the rates in the Northeast and West. The homeownership rates in the Midwest, South, and West were higher than the rates in the third quarter of 2019, while the rate in the Northeast was not statistically different.

US Housing Market Summary For January 2021

The housing market before the pandemic was remarkably strong. The coronavirus crisis response was unprecedented. The federal government ordered a de facto shutdown of the entire private economy, closing an estimated eighty percent of businesses. It has caused unemployment to soar to at least ten percent, while tens of millions are idled.

According to the National Association of Realtors®, overall sales decreased year-over-year, down 17.2% (4.33 million units in April 2020) from a year ago (5.23 million in April 2019). The national median existing single-family home price in the first quarter of 2020 was $274,600, up 7.7% from the first quarter of 2019 ($254,900). Housing market data of the last month showed that it is beginning to heat up again as more sellers and buyers enter the market.

Realtor.com’s latest national housing report shows that listing price growth continued to increase at double-digit rates compared to last year. Homes continued to sell almost two weeks more quickly than last year. Inventory continues to decrease, still posing a challenge for buyers. Buyers will face a competitive spring season as sellers slowly crawl back into the market and inventory remains low. Homebuyers may need to prepare for a competitive season with lower inventory (especially in more affordable price categories), continuing growth in asking prices in response to strong buyer demand, and slowly rising interest rates.

Housing Market Trends For Supply

Nationally, the inventory of homes for sale in January decreased by 42.6% over the past year, a higher rate of decline compared to the 39.6% drop in December. This amounted to 443,000 fewer homes for sale compared to January of last year. Despite a slightly more active December, sellers once again entered the market more hesitantly in January, which saw 23.2% fewer new listings enter the market compared to last year.

A declining inventory suggests that buyers are more active than sellers, perhaps looking to lock-in record-low mortgage rates. The total housing supply is not enough to mark it as a buyer’s real estate market and it going to continue to be difficult for buyers to find their perfect home, while sellers who face little competition amongst each other may find selling their home easier this fall season than is typical.

Housing inventory in the 50 largest U.S. metros overall declined by 41.8% over last year in January, greater than last month’s 38.6% decline. While in December, all regions except for the South saw a year-over-year increase in new listings, in January, all regions saw renewed declines as sellers became skittish entering into 2021. New listings were down 24.0% in the South, 22.6% in the Midwest, 14.4% in the Northeast, and 6.6% in the West.

Housing markets that saw the largest year-over-year decline in newly listed homes included Cleveland (-37.1%), Jacksonville (-36.9%), and Memphis (-32.6%). Only San Jose, San Francisco, and Denver saw newly listed homes increase, by 24.8% and 14.4%, and 1.8%, respectively. Overall, newly listed homes in the largest 50 metros decreased by 17.3% compared to last year.

According to the National Association of Realtors®, total housing inventory at the end of December totaled 1.07 million units, down 16.4% from November and down 23% from one year ago (1.39 million). Unsold inventory sits at an all-time low 1.9-month supply at the current sales pace, down from 2.3 months in November and down from the 3.0-month figure recorded in December 2019. For existing single-family homes, the unsold inventory sits are 2.2 months.

| Total housing inventory at the end of December totaled 1.07 million units, down 16.4% from November and down 23% from one year ago (1.39 million). |

| Total housing inventory at the end of November totaled 1.28 million units, down 9.9% from October and down 22% from one year ago (1.64 million). |

| Total housing inventory at the end of October totaled 1.42 million units, down 2.7% from September and down 19.8% from one year ago (1.77 million). |

| Total housing inventory at the end of September totaled 1.47 million units, down 1.3% from August and down 19.2% from one year ago (1.82 million). |

| Total housing inventory at the end of August totaled 1.49 million units, down 0.7% from July and down 18.6% from one year ago (1.83 million). |

| Total housing inventory at the end of July totaled 1.50 million units, down from both 2.6% in June and 21.1% from one year ago (1.90 million). |

| Total housing inventory at the end of June totaled 1.57 million units, up 1.3% from May, but still down 18.2% from one year ago (1.92 million). |

| Total housing inventory at the end of May totaled 1.55 million units, up 6.2% from April, and down 18.8% from one year ago (1.91 million). |

| Total housing inventory at the end of April totaled 1.47 million units, down 1.3% from March, and down 19.7% from one year ago (1.83 million). |

Housing Market Trends For Listing Prices

Realtor.com’s data shows that the median national home listing price grew by 15.4% over last year, to $346,000 in January, higher than last month’s growth rate of 13.4%. Listing prices in the nation’s largest metros grew by an average of 10.9% compared to last year, higher than last month’s rate of 8.8%.

In October, the median listing price held steady at the summer 2020 high of $350,000, resisting the usual seasonal decline for the first time in Realtor.com’s recorded data history. Had there been no pandemic this year, prices would have normally dropped 1-4% from summer’s price peak by October.

The nation’s median listing price per square foot also grew by 17.5% compared to last year, an acceleration from the 15.9% growth seen last month. In May, the nation’s median listing price growth had deaccelerated, driven by diminished seller expectations and a shift in the mix of homes for sale.

According to the National Association of Realtors®, the median sales price for all existing housing types in December was $309,800, up 12.9% from December 2019 ($274,500). Home prices increased in every region and December’s national price increase marks 106 straight months of year-over-year gains.

The following is a tabulated summary of the National Listing Price Trends from March 2020 to January 2021 on Realtor.com.

National Housing Price Trends 2020 – 2021 |

| In the first two weeks of March, the median listing prices were increasing 4.4 percent year-over-year on average. |

| The median list price on pending contracts in the four weeks through April 26 was up 2.6% from one year ago. |

| The April national median listing price was $320,000, up 0.6 percent year-over-year. |

| This was a further deceleration from the 3.8 percent year-over-year growth seen in March. |

| In the three weeks of May ending May 9, May 16, and May 23, the median national listing price posted an increase of 1.4 percent, 1.5 percent, and 3.1 percent year-over-year, respectively. |

| Locally, 77 of 100 large metros saw asking prices increase over last year. |

| In May 2020, the median national home listing price grew by 1.6 percent year-over-year, to a new high of $330,000. |

| This is a re-acceleration from the 0.6 percent year-over-year growth seen in April. |

| In June, the median national home listing price grew by 5.1 percent year-over-year, to a new high of $342,000. |

| This is an acceleration from the 1.6 percent year-over-year growth seen in May. |

| The nation’s median listing price per square foot also grew by 7.7 percent year-over-year, an acceleration from the 5.4 percent growth seen last month. |

| The July national median listing price was $349,000, up 8.5 percent year-over-year. Prices rose 7.8 percent in larger markets. |

| This is an acceleration from the 5.1 percent year-over-year growth seen in June. |

| The nation’s median listing price per square foot also grew by 9.5 percent year-over-year, an acceleration from the 7.7 percent growth seen in June. |

| The median national home listing price grew by 10.1 percent year-over-year, to a new high of $350,000 in August. |

| This is an acceleration from the 8.5 percent year-over-year growth seen in July. |

| The median national home listing price grew by 11.1% over last year, to $350,000 in September. |

| This is an acceleration from the 10.1% growth seen in August. |

| The nation’s median listing price per square foot also grew by 13.9% compared to last year. |

| In October, the median national home listing price grew by 12.2% over last year, to $350,000. |

| This is an acceleration from the 11.1% growth seen in September. |

| The nation’s median listing price per square foot also grew by 14.7% compared to last year. |

| In November, the median national home listing price grew by 12.7 percent year-over-year, to $348,000. |

| The nation’s median listing price per square foot also grew by 15.4% compared to last year. |

| In December, the median national home listing price grew by 13.4 percent year-over-year, to $340,000. |

| The nation’s median listing price per square foot also grew by 15.9% compared to last year. |

| In January 2021, the median national home listing price grew by 15.4 percent year-over-year, to $346,000. |

| The nation’s median listing price per square foot also grew by 17.5% compared to last year. |

Among the largest 50 metros, listing prices are increasing most in northeastern markets, where they are now growing at an average rate of 16.8% over last year, compared to a growth rate of 12.3% for western metros, 10.4% for midwestern metros, and 8.0% for southern metros. This month, price growth accelerated in all regions compared to last month.

Austin (+30.2%), Rochester (25.9%), and Los Angeles (+22.4%) posted the highest year-over-year median list price growth in January. Miami (-3.2% year-over-year) and Minneapolis (-0.4%) were the only top 50 metros to see listing prices decline year-over-year in January.

| Highest Year-Over-Year Price Gains | Highest Year-Over-Year Price Declines | |

| May | Los Angeles-Long Beach-Anaheim, CA (+14.9%) | Detroit-Warren-Dearborn, MI (-3.4%) |

| Pittsburgh, PA (+14.0%); and Cincinnati, OH-KY-IN (+12.1%) | San Antonio-New Braunfels, TX (-3.2%) | |

| — | Seattle-Tacoma-Bellevue, WA (-3.1%) | |

| June | Pittsburgh, PA (+23.8%) | Miami-Fort Lauderdale-West Palm Beach, FL (-2.3%) |

| Los Angeles-Long Beach-Anaheim, CA (+21.4%) | Jacksonville, FL (-0.8%) | |

| Cincinnati, OH-KY-IN (+16.6%) | Dallas-Fort Worth-Arlington, TX (-0.7%) | |

| July | Pittsburgh, PA (+25.0%) | Miami-Fort Lauderdale-West Palm Beach, FL (-1.5%) |

| Los Angeles-Long Beach-Anaheim, CA (+24.3%) | Orlando-Kissimmee-Sanford, FL (-0.9%) | |

| Cincinnati, OH-KY-IN (+18.5%) | — | |

| August | Philadelphia-Camden-Wilmington, PA-NJ-DE-MD (+18.6 percent) | Miami-Fort Lauderdale-West Palm Beach, FL (-0.2 percent) |

| Cincinnati, OH-KY-IN (+17.8 percent) | — | |

| Cleveland-Elyria, OH (+15.6 percent) | — | |

| September | Cincinnati, OH-KY-IN (+16.9%) | — |

| Boston-Cambridge-Newton, MA-NH (+16.4%) | — | |

| Philadelphia-Camden-Wilmington, PA-NJ-DE-MD (+15.6%) | — | |

| October | Los Angeles (+16.9%) | — |

| Philadelphia (+16.7%) | — | |

| Cincinnati (16.3%) | — | |

| November | Austin (+20.0%) | — |

| Los Angeles (+16.1%) | — | |

| Riverside-San Bernardino (15.9%) | — | |

| December | Austin (+16.9%) | Minneapolis (-1.6%) |

| Riverside-San Bernardino (17.2%) | — | |

| New Orleans (+16.8%) | — | |

| January 2021 | Austin (+30.2%) | Miami (-3.2%) |

| Rochester (25.9%) | Minneapolis (-0.4%) | |

| Los Angeles (+22.4%) | — |

Housing Market Trends For Sales

Homes for sale in January 2021 were being scooped up more quickly than last year as buyer demand remained solid through the new year. The typical home spent 76 days on the market this January, which is 10 days less than last year. However, this yearly decline has slowed compared to December 2020, when homes sold 13 days more quickly than the previous year.

In the 50 largest U.S. metros, the typical home spent 60 days on the market, and homes spent 12 days less on the market, on average, compared to last January. Among these 50 largest metros, the time a typical property spends on the market has decreased most in the South and West, where the typical property spent 2 weeks less on the market compared to last year, followed by the Midwest (-12 days) and the Northeast (-11 days).

Among larger metropolitan areas, homes saw the greatest decline in time spent on the market compared to last year in Virginia Beach (-27 days); Sacramento (-24 days); and Birmingham (-22 days). Only two markets saw time on the market increase compared to the previous year: New York (+11 days), and Miami (+5 days).

Existing-home sales rose in December, with home sales in 2020 reaching their highest level since 2006, according to the National Association of Realtors®. Activity in the major regions was mixed on a month-over-month basis, but each of the four areas recorded double-digit year-over-year growth in December.

Total existing-home sales completed transactions that include single-family homes, townhomes, condominiums, and co-ops, increased 0.7% from November to a seasonally-adjusted annual rate of 6.76 million in December. Sales in total rose year-over-year, up 22.2% from a year ago (5.53 million in December 2019).

| Housing Sales By Region – December 2020 (By N.A.R.) | ||||||||

| Northeast | Existing home sales climbed 4.5%, recording an annual rate of 930,000, a 27.4% increase from a year ago. | |||||||

| The median price in the Northeast was $362,100, up 19.0% from December 2019. | ||||||||

| Midwest | Existing-home sales were unchanged, recording an annual rate of 1,590,000 in December, but up 26.2% from a year ago | |||||||

| The median price in the Midwest was $235,700, a 13.7% increase from December 2019. | ||||||||

| South | Existing-home sales increased 1.1% to an annual rate of 2,860,000 in December, up 20.7% from the same time one year ago. | |||||||

| The median price in the South was $268,100, an 11.3% increase from a year ago. | ||||||||

| West | Existing-home sales fell 1.4% from the month prior, recording an annual rate of 1,380,000 in December, a 17.9% increase from a year ago. | |||||||

| The median price in the West was $467,900, up 14.2% from December 2019. | ||||||||

First-time buyers were responsible for 31% of sales in December, unchanged from the same time in 2019, but down from 32% in November 2020. Individual investors or second-home buyers, who account for many cash sales, purchased 14% of homes in December, identical to the share recorded in November 2020 and a small decline from 17% in December 2019.

All-cash sales accounted for 19% of transactions in December, down from 20% in both November and December 2019. Distressed sales – foreclosures and short sales – represented less than 1% of sales in December, equal to November’s percentage but down from 2% in December 2019.

Despite dropping slightly in the last month of 2020, the latest pending home sales registered as the highest ever recorded in December, according to the National Association of Realtors®. The decrease marks the fourth consecutive month of month-over-month declines. While contract transitions fell in one of the four major U.S. regions, activity climbed or remained flat in the three other areas. Compared to a year ago, all four regions witnessed double-digit gains in pending home sales transactions.

Pending home sales fell slightly in October, according to the National Association of Realtors. Contract activity was mixed among the four major U.S. regions, with the only positive month-over-month growth happening in the South, although each region achieved year-over-year gains in pending home sales transactions. All regions experienced double-digit year-over-year increases.

NAR’s Pending Home Sales Index (PHSI), fell 0.3% to 125.5 in December. Year-over-year, contract signings jumped 21.4%. An index of 100 is equal to the level of contract activity in 2001. The Northeast PHSI rose 3.1% to 112.0 in December, a 22.1% increase from a year ago. In the Midwest, the index fell 3.6% to 111.7 last month, up 13.9% from December 2019.

Pending home sales in the South increased 0.1% to an index of 150.6 in December, up 26.6% from December 2019. The index in the West was unchanged in December, remaining at 111.3, which is up 18.9% from a year ago.

Housing Market Forecast 2021: Will This Boom Continue?

With 10 years having now passed since the Great Recession, the U.S. has been on the longest period of continued economic expansion on record. The housing market has been along for much of the ride and continues to benefit greatly from the overall health of the economy. However, hot economies eventually cool and with that, hot housing markets move more towards balance.

With 10 years having now passed since the Great Recession, the U.S. has been on the longest period of continued economic expansion on record. The housing market has been along for much of the ride and continues to benefit greatly from the overall health of the economy. However, hot economies eventually cool and with that, hot housing markets move more towards balance.

The housing market 2020 was running at a record pace in the early stages of the coronavirus outbreak in February 2020, with sellers continuing to gain leverage, and buyers benefit from lower mortgage rates. We saw some of the best home sales and housing starts to pace in more than a decade until February 2020.

Before the COVID-19 pandemic, Realtor.com’s national housing forecast for 2020 was that home price growth will flatten, with an expected increase of 0.8 percent. Inventory was predicted to remain constrained, especially at the entry-level price segment. Mortgage rates were predicted to likely bump up to 3.88 percent by the end of the year.

Buyers were expected to continue to move to affordability, benefiting smaller and mid-sized markets. The housing market predictions were pointing out that all the housing indices would trend upward for the nation as a whole as well as in every state, including the top 100 metro areas.

After the coronavirus pandemic came into being, the housing market forecast runs the gamut from optimistic to pessimistic. The fall in GDP associated with the coronavirus pandemic, and the rise in unemployment, was unprecedented. As the number of coronavirus cases grew and lockdowns began taking effect across the United States, real estate activity slowed dramatically. Both buyers and sellers pulled back from the housing market.

According to Zillow, after the third week of March, newly pending sales dropped each week through mid-April, hitting a low of 38.8% below 2019’s figures in a time period when sales usually heat up. Time on the market grew to three days longer than last year in early May, while list price appreciation fell to just 0.1% above 2019.

Year-over-year rent growth in the U.S. saw the biggest one-month slowdown in at least five years. About 3 million adults moved in with their parents or grandparents in April, bringing the number of adults living at home to the highest number on record.

Despite all of that, there were no signs that the housing market is about to subside. The housing market absorbed the shock relatively quickly and began to recover. Pent-up demand that was put on hold was unleashed starting in late April, then supercharged by even lower mortgage rates and changes in housing needs.

Annual growth in median sale prices peaked at 7.4% the second week of April, before plummeting in the early days of the market freeze and falling to 0.8% by late May. But after the freeze began to thaw, year-over-year growth rose sharply and steadily, hitting new highs of 13.8% by late October, according to Zillow’s data.

Before the pandemic hit the nation the supply of new housing was failing to keep up with demand. Although buyers were eager to close on houses, sellers were not so anxious to list their houses. Inventory was low compared to 2019 to start the year, and that gap widened nearly every week through early December.

Due to a very tight inventory, coupled with strong demand from first-time buyers, the housing market began to move incredibly fast. Sellers who did choose to list had little trouble finding motivated buyers who were looking to take advantage of low-interest rates. After peaking in early May, time on the market began to fall through early November as available homes for sale were scooped up faster.

According to Zillow, in September 2020, one in five houses sold above list price – about 50% more than long-term norms. Houses’ typical time on the market reached down to 12 days in October — selling at blazing speeds regardless of price. By November, home values had risen 1.1% since October and 3% since the previous quarter — the largest monthly and quarterly gains in Zillow records going back to 1996.

Inventory declined every week starting in early June – by the week ending Dec. 12, it was 34.3% below 2019 levels. As of the week of Dec. 12, houses were typically on the market a median of just 16 days before an offer was accepted — up a handful of days from lows set in earlier weeks, but still a full three weeks (21 days) less than the same time last year.

Zillow expected that 5.7 million existing homes will be sold by the end of 2020, up 5.9% from 2019. This prediction turned out to be true. 2020 was a record-breaking year in residential real estate. But while 2020 will end up being a strong year for the housing market by most measures, it will pale in comparison to 2021.

Zillow predicts that almost 6.9 million existing homes will be sold in the calendar year 2021, the most sales recorded in a single calendar year since 2005 and the largest one-year increase (21.9%) since the early 1980s. According to some experts, the economic cost we’ve paid to try to contain the virus will weigh down the economy into 2021. That is why home sales are expected to be around six million in 2021 instead of the previously projected 6.3 million.

Economic sentiment affected the U.S. housing market, too. People were reluctant or unable to show their homes, while others are afraid it won’t sell and thus didn’t list their homes at all. Recovery is also expected to be uneven. Housing markets that are more heavily impacted should expect a slower recovery than markets that were hit less severely.

If you’re wondering what the state of the housing market will be like over the next six months, especially if you’re an investor, then here is some good news for you. The mismatch between supply and demand is driving prices higher, but this isn’t a housing bubble. Economic sentiment affected the U.S. housing market, too.

Many experts were predicting that the pandemic could lead to a housing crash worse than the great depression. But that’s not going to happen. The market is in much better shape than a decade ago. The housing market is well past the recovery phase and is now booming with higher home sales compared to the pre-pandemic period.

Let’s first look at one of the most talked-about negative housing forecasts for 2021 — The rising mortgage delinquencies and their impact on the housing market in 2021? MBA forecasts that the refinance boom will surge in March and then drop by 54% by the second quarter of 2021.

Delinquencies at the end of 2019 were at their lowest level since 1979. That turned around quickly with the pandemic and spike in unemployment. It is important to note that foreclosure activity is increasing despite the various foreclosure moratoria that are in place. Mortgage delinquencies and foreclosures increased in August and October, respectively. 1.2% of loans are at least 150 days past due according to CoreLogic.

ATTOM reported that foreclosures increased by 20% in October. The increased long-term delinquency is due to participation in forbearance programs, and foreclosures are down 80% year-over-year. South Carolina, Nebraska, and Alabama post the highest state foreclosure rates